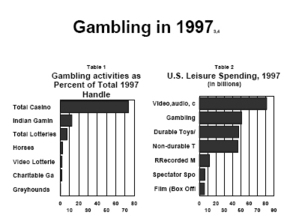

Each year, a major trade publication of the gambling industry releases a supplement to its monthly publication. The magazine, International Gaming & Wagering Business, features advertisements for roulette wheels and slot machines nestled between articles about the future of the lottery in India and horse racing in the United Kingdom [1]. The United States Gross Annual Wager, the annual supplement, serves as a state-of-the-industry report and provides various gambling data and indices. This year’s report opens with this observation, “American gambling appetites are satiated. Casinos excepted, Americans now have all the gambling they want. The economy is booming, but consumer spending on commercial games was up by just 6.2%…” [2]. But stopping at the first paragraph would be to ignore some of the report’s more interesting findings. The tables below provide a more nuanced portrait of American gaming habits. Much of the report is explicated using industry jargon; one definition in particular is worth noting. Several IGWB charts refer to the “handle” of a particular activity, meaning the total gross amount gambled. Thus, the handle for a slot machine on any given night is the total value of all money (or its equivalent) spent by gamblers on that particular machine on that given night.

However dire-sounding the IGWB’s opening caveat, gambling is still very much a part of the American economy. It should be noted that a low growth rate in comsumer spending on gaming does not necessarily signify a decline in gambling activities. Other economic indicators such as inflation should be considered, as should the growth rates of other leisure expenditures. Table 1 reveals the relative contribution that selected gaming activities make toward the total $638,598,900,000 handle for 1997.

Sources:

- (1998, August). International Gaming & Wagering Business 19(8).

- (1998, August). The United States Gross Annual Wager, supplement to International Gaming and Wagering Business 19(8)3.

- (Table 1) ibid. 7.

- (Table 2) ibid. 17.